Organisation, Management and Control Mode ex d.lgs. N. 231/2001

01. CRIMINAL LIABILITY OF ENTITIES

1.1. The legal regime of the criminal liability of entities

Legislative Decree no. 231 of 8 June 2001 regulates the criminal liability of entities deriving from crimes committed by persons connected to them, introducing it for the first time into the national legal system.

The Entity is called upon to respond in the event that a person who is part of its organization (administrator, manager, employee, collaborator, etc.) commits one of the crimes provided for by Decree 231/01, in the interest or to the advantage of the Entity itself.

In particular, the decree provides for the liability of the entity if the crime is committed, in its interest or to its advantage by:

- natural persons who hold top positions, so-called "top management" (representation, administration or management of the entity or another organizational unit or persons who exercise, in fact, management and control);

- natural persons subject to the direction or supervision by one of the above-mentioned subjects.

As for the type of crimes provided for by the Decree, it should be emphasized that originally the liability of the entity was provided only for certain forms of crime against the "public administration", subsequently the text of the Decree was extended to include much broader cases.

To date, the decree provides for the liability of entities for:

Crimes against the public administration, such as:

- undue receipt of contributions, loans or other disbursements from the State or other public body (Article 316 ter of the Criminal Code);

- fraud to the detriment of the State or other public body or of the European Communities (Article 640, paragraph 2, para., no. 1, of the Criminal Code);

- embezzlement to the detriment of the State or other public body (Article 316 bis of the Criminal Code);

- aggravated fraud for the achievement of public disbursements (Article 640 bis of the Criminal Code);

- computer fraud to the detriment of the State or other public body (Article 640 ter of the Criminal Code);

- crimes of fraud in public procurement (Article 356 of the Criminal Code);

- crimes of fraud in public supplies also to the detriment of the European Union and fraud in agriculture (art. 2 l. 898/1986 and subsequent amendments);

- disturbed freedom of enchantments (Article 353 of the Criminal Code);

- disturbed freedom of the procedure for choosing the contractor (Article 353-bis of the Criminal Code);

- trafficking in illicit influence (Article 346-bis of the Criminal Code as amended by Law 114/2024);

- improper use of money or movable property;

- undue inducement to give or promise benefits.

Fraud in sports competition, abusive exercise of gaming or betting and games of chance exercised by means of prohibited machines (art. 25-quaterdecies of Legislative Decree 231/2001), as introduced by art. 5 of Law no. 39 of 03.05.2019;

Corruption crimes, such as:

- corruption (Articles 318, 319, 319-bis and 321 of the Criminal Code);

- bribery (Article 317 of the Criminal Code);

- corruption in judicial acts (Article 319 ter of the Criminal Code);

- corruption of a person in charge of public service (Article 320 of the Criminal Code);

- embezzlement, bribery, undue inducement to give or promise benefits, corruption and incitement to corruption, abuse of office, of members of international courts or bodies of the European Communities or international parliamentary assemblies or international organizations and officials of the European Communities and foreign States (Article 322-bis of the Criminal Code); undue inducement to give or promise benefits (Article 319 quarter of the Criminal Code);

- incitement to corruption (Article 322 of the Criminal Code);

- crimes of embezzlement (Article 314 of the Criminal Code);

- undue use of money or movable property (Article 314-bis of the Criminal Code);

- embezzlement by profiting from the error of others (Article 316 of the Criminal Code);

- Trafficking in illicit influence (Article 346-bis of the Criminal Code).

Corporate crimes, such as:

- false corporate communications (Article 2621 of the Italian Civil Code);

- false corporate communications for minor facts (Article 2621 bis of the Italian Civil Code);

- false corporate communications of listed companies (Article 2622 of the Italian Civil Code);

- impeded control (Article 2625, paragraph 2, of the Italian Civil Code);

- false prospectus (art. 2623 par. 1 and 2, c.c.);

- falsehoods in the reports or communications of auditing firms (Article 2624 paragraphs 1 and 2, of the Italian Civil Code);

- undue restitution of contributions (Article 2626 of the Italian Civil Code);

- illegal distribution of profits and reserves (Article 2627 of the Italian Civil Code);

- unlawful transactions on the shares or quotas of the parent company (Article 2628 of the Italian Civil Code);

- transactions in the prejuition of creditors (Article 2629 bis of the Italian Civil Code);

- fictitious formation of capital (Article 2632 of the Italian Civil Code);

- undue distribution of company assets by liquidators (Article 2633 of the Italian Civil Code);

- unlawful influence on the shareholders' meeting (Article 2636 of the Italian Civil Code);

- rigging (art. 2637 of the Italian Civil Code);

- obstruction of the exercise of the functions of public supervisory authorities (Article 2638, paragraphs 1 and 2 of the Italian Civil Code);

- corruption between private individuals (Article 2635 of the Italian Civil Code);

- incitement to corruption between private individuals (Article 2635 bis of the Italian Civil Code);

- false or omitted declarations for the issuance of the preliminary certificate provided for by the implementing legislation of Directive (EU) 2019/2121, of the European Parliament and of the Council of 27 November 2019 (Articles 54, 55 of Legislative Decree 19/2023).

Crimes of insider dealing and manipulation of the financial market (so-called market abuse), such as:

- abuse or unlawful disclosure of inside information, recommendation or inducement of others to commit insider dealing (Legislative Decree 58/1998 art. 184);

- market manipulation (Legislative Decree 58/98 art. 185).

Offences relating to counterfeiting of coins, public credit cards, revenue stamps and identification instruments or signs, such as:

- counterfeiting of coins, spending and introduction into the state, subject to agreement, of counterfeit coins (Article 453 of the Criminal Code);

- alteration of coins (Article 454 of the Criminal Code);

- spending and introduction into the State, without concert, of counterfeit coins (Article 455 of the Criminal Code);

- spending of counterfeit coins received in good faith (Article 457 of the Criminal Code);

- falsification of revenue stamps, introduction into the State, purchase, possession or putting into circulation of falsified revenue stamps (Article 459 of the Criminal Code);

- counterfeiting of watermarked paper used for the manufacture of public credit cards or revenue stamps (Article 460 of the Criminal Code);

- manufacture or possession of watermarks or instruments intended for the counterfeiting of coins of revenue stamps or watermarked paper (Article 461 of the Criminal Code);

- use of counterfeit or altered revenue stamps (Article 464 of the Criminal Code);

- counterfeiting, alteration or use of trademarks or distinctive signs, or patents, models and designs (Article 473 of the Criminal Code);

- introduction into the state and trade in counterfeit products (Article 474 of the Criminal Code).

- Offences committed for the purpose of terrorism or subversion of the democratic order, provided for by the penal code and special laws, as well as carried out in violation of the New York Convention of 9 December 1999.

Offences against the individual's personality, such as:

- reduction or maintenance in slavery or servitude (Article 600 of the Criminal Code);

- child prostitution (Article 600 bis of the Criminal Code);

- child pornography (Article 600 ter of the Criminal Code);

- possession of or access to pornographic material (Article 600 quarter of the Criminal Code);

- virtual pornography (Article 600 quarter 1 of the Criminal Code);

- tourist initiatives aimed at the exploitation of child prostitution (Article 600 quinquies of the Criminal Code);

- solicitation of minors (Article 609 undecies of the Criminal Code);

- trafficking in persons (Article 601 of the Criminal Code);

- purchase and alienation of slaves (Article 602 of the Criminal Code);

- illegal intermediation and exploitation of labour (Article 603-bis of the Criminal Code).

Practices of mutilation of female genital organs (Article 583-bis of the Criminal Code).

Manslaughter and serious or very serious culpable injuries, committed in violation of accident prevention regulations and on the protection of hygiene and health at work (Articles 589 and 590 c.3 of the Criminal Code).

Receiving stolen goods, laundering and use of money, goods or utilities of illegal origin as well as self-laundering pursuant to art. 25-octies of Legislative Decree no. 231/2001, as amended by Legislative Decree no. 195/2021 transposing EU Directive 2018/1673, in particular:

- receiving stolen goods (Article 648 of the Criminal Code);

- money laundering (Article 648-bis of the Criminal Code);

- use of money, goods or utilities of illicit origin (Article 648-ter of the Criminal Code);

- self-laundering (Article 648-ter.1 of the Criminal Code).

Computer crimes and unlawful data processing, as amended by Law 90/2024 such as:

- abusive access to a computer or telematic system (Article 615-ter of the Criminal Code);

- illegal possession, dissemination and installation of equipment, codes and other devices suitable for access to computer or telematic systems (Article 615-quarter of the Criminal Code);

- illegal possession, dissemination and installation of equipment, devices or information programs aimed at damaging or interrupting an IT or telematic system (Article 615-quarter.1 of the Criminal Code);

- unlawful interception, impediment or interruption of computer or telematic communications (Article 617-quarter of the Criminal Code);

- illegal possession, dissemination and installation of equipment and other means to intercept, prevent or interrupt computer or telematic communications (Article 617-quinquies of the Criminal Code);

- computer extortion (Article 629 paragraph 3 of the Criminal Code);

- damage to information, data and computer programs (Article 635-bis of the Criminal Code);

- damage to information, data and computer programs used by the State or by another public body or in any case of public utility (Article 635-ter of the Criminal Code);

- damage to computer or telematic systems (Article 635-quarter of the Criminal Code);

- illegal possession, dissemination and installation of equipment, devices or computer programs aimed at damaging or interrupting an IT or telematic system (Article 635-quarter.1 of the Criminal Code);

- damage to information or telematic systems of public utility (Article 635-quinquies of the Criminal Code);

- electronic documents (Article 491 bis of the Criminal Code);

- computer fraud of the entity providing electronic signature certification services (Article 640-quinquies of the Criminal Code);

- crimes in the field of national security and cybernetics (art. 1, paragraph 11, of Legislative Decree no. 105 of 21 September 2019).

Organized crime crimes, such as:

- criminal conspiracy (Article 416 of the Criminal Code);

- mafia-type associations, including foreign ones (Article 416 bis of the Criminal Code);

- political-mafia electoral exchange (Article 416-ter);

- kidnapping for the purpose of extortion (Article 630 of the Criminal Code);

- association aimed at the illicit trafficking of narcotic or psychotropic substances (art. 74 Presidential Decree 9 October 1990, no. 309);

- Illegal manufacture, introduction into the State, offering for sale, transfer, possession and carrying in a public place or place open to the public of weapons of war or war-type weapons or parts thereof, explosives, clandestine weapons as well as several common firearms excluding those provided for in Article 2, third paragraph, of Law No. 110 of 18 April 1975 (Article 407, paragraph 2, letter a), number 5), c.p.p.).

Transnational crimes, provided for by Law no. 146 of 16 March 2006, arts. 3 and 10.

Crimes against industry and commerce, such as:

- disturbed freedom of industry or commerce (Article 513 of the Criminal Code);

- unlawful competition with threat or violence (Article 513 bis of the Criminal Code);

- fraud against national industries (Article 514 of the Criminal Code);

- fraud in the exercise of trade (Article 515 of the Criminal Code);

- sale of non-genuine foodstuffs as genuine (Article 516 of the Criminal Code);

- sale of industrial products with false signs (Article 517 of the Criminal Code as amended by Law 206/2023);

- counterfeiting of geographical indications or designations of origin of agri-food products (Article 517 quarter of the Criminal Code);

- manufacture and trade of goods made by usurping industrial property rights (Article 517-ter of the Criminal Code).

Offences relating to the infringement of copyright referred to in art. 25 novies (Articles 171 c. 1 L.a)-bis and c.3, 171 bis, 171 ter, 171 septies and 171 octies of Law No. 633 of 22 April 1941, as amended by Law 93/2023 and Law No. 166/2024).

Inducement not to make declarations or to make false declarations to the judicial authority (Article 377-bis of the Italian Civil Code).

Environmental Crimes, as amended by Legislative Decree 116/2025 conv. in Law 147/2025, such as:

- killing, destruction, capture, removal, possession of specimens of protected wild animal or plant species (Article 727-bis of the Criminal Code);

- destruction or deterioration of habitats within a protected site (Article 733-bis of the Criminal Code);

- import, export, possession, use for profit, purchase, sale, exhibition or possession for sale or for commercial purposes of protected species (art. 1 c. 1 and 2, art. 2 c. 1 and 2, art. 6 c. 4, art. 3 bis L. 150/92);

- intentional or negligent pollution caused by ships (art. 9 c. 1 and 2, art. 8 c. 1 and 2 Legislative Decree 202/07);

- ozone-depleting substances (art. 3 c. 6 L. 549/1993);

- integrated environmental authorisation (art. 29-quattuordecies of Legislative Decree 152/2006);

- emissions into the atmosphere (art. 279 of Legislative Decree 152/2006);

- discharges of industrial waste water containing hazardous substances; discharges into the soil, subsoil and groundwater;

- discharge into sea waters by ships or aircraft (art. 137 Legislative Decree 152/06);

- failure to remediate as a result of pollution of the soil, subsoil, surface water or groundwater (art. 257 c. 1 and 2 of Legislative Decree 152/06);

- unauthorised waste management activities (Article 256 of Legislative Decree 152/06);

- violation of the obligations of communication, keeping of mandatory registers and forms (art. 258 of Legislative Decree 152/06);

- illegal trafficking of waste (art. 259 of Legislative Decree 152/06);

- organised activities for the illegal trafficking of waste (Article 452-quaterdecies of the Criminal Code);

- false indications on the nature, composition and chemical-physical characteristics of waste in the preparation of a waste analysis certificate;

- inclusion in SISTRI of a false waste analysis certificate;

- omission or fraudulent alteration of the paper copy of the SISTRI form - handling area in the transport of waste (art. 260-bis Legislative Decree 152/06);

- intentional and negligent pollution (Legislative Decree no. 202 of 2007 articles 8 and 9);

- environmental pollution (Article 452 bis of the Criminal Code);

- environmental disaster (Article 452 quarter of the Criminal Code);

- culpable crimes against the environment (Article 452 quinquies of the Criminal Code);

- trafficking and abandonment of highly radioactive material (Article 452 sexies of the Criminal Code);

- aggravating circumstances, aggravated associative crimes (Article 452 octies of the Criminal Code);

- impeded control (Article 425-septies of the Criminal Code);

- failure to remediate (Article 452-terdecies of the Criminal Code);

- organized activities for the illegal trafficking of waste;

- abandonment of non-hazardous waste in special cases (Article 255-bis of Legislative Decree 152/06);

- abandonment of hazardous waste (art. 255-ter of Legislative Decree 152/06);

- illegal combustion of waste (art. 256-bis of Legislative Decree 152/06);

- culpable crimes in the field of waste (art. 259-ter of Legislative Decree 152/06).

Use of illegally staying third-country nationals, in relation to the offences referred to in Articles:

- 22, c. 12 bis, Legislative Decree no. 286 of 25 July 1998 (Immigration Act) - fixed-term and open-ended employment;

- 12, c. 3, 3-bis, 3-ter and 5 of Legislative Decree no. 286 of 25 July 1998 - Provisions against illegal immigration.

Racism and xenophobia, in relation to the crimes referred to in Article 604 bis of the Criminal Code, entitled "propaganda and incitement to crime for reasons of racial, ethnic and religious discrimination".

Tax crimes, such as:

- crime of fraudulent declaration by means of other artifices (Article 3 of Legislative Decree no. 74 of 10 March 2000);

- crime of fraudulent declaration through the use of invoices or other documents for non-existent transactions (art. 2 Legislative Decree no. 74/2000);

- crime of issuing invoices or other documents for non-existent transactions (Article 8 of Legislative Decree no. 74 of 10 March 2000);

- crime of concealment or destruction of accounting documents (Article 10 of Legislative Decree No. 74 of 10 March 2000);

- crime of fraudulent evasion of the payment of taxes (Article 11 of Legislative Decree No. 74 of 10 March 2000);

- crime of unfaithful declaration (art. 4 of Legislative Decree 74/2000);

- crime of failure to declare (art. 5 of Legislative Decree 74/2000);

- offence of undue compensation (Article 10-quarter of Legislative Decree 74/2000).

Offences relating to the violation of restrictive measures of the European Union referred to in art. 25-octies.2 of Legislative Decree 231/2001, as introduced by Legislative Decree 211/2025, such as:

- violation of the restrictive measures of the European Union (Article 275-bis of the Criminal Code);

- violation of information obligations imposed by an EU restrictive measure (Article 275-ter of the Criminal Code);

- violation of the conditions of the authorization to carry out activities (Article 275-quarter of the Criminal Code).

Smuggling offences, such as:

- smuggling in the movement of goods across land borders and customs areas (Article 282 of Presidential Decree 43/1973);

- smuggling in the movement of goods in border lakes (art. 283 of Presidential Decree 43/1973);

- smuggling in the maritime movement of goods (art. 284 of Presidential Decree 43/1973);

- smuggling in the movement of goods by air (Article 285 of Presidential Decree 43/1973);

- smuggling in non-customs areas (art. 286 of Presidential Decree 43/1973);

- smuggling for undue use of goods imported with customs facilities (Article 287 of Presidential Decree 43/1973);

- smuggling into customs warehouses (Article 288 of Presidential Decree 43/1973);

- smuggling in cabotage and circulation (Article 289 of Presidential Decree 43/1973);

- smuggling in the export of goods eligible for the refund of duties (Article 290 of Presidential Decree 43/1973);

- smuggling in the temporary import or export (art. 291 of Presidential Decree 43/1973);

- smuggling of foreign manufactured tobacco (Article 291-bis of Presidential Decree 43/1973);

- aggravating circumstances of the crime of smuggling foreign manufactured tobacco (Article 291-ter of Presidential Decree 43/1973);

- criminal conspiracy aimed at smuggling foreign manufactured tobacco (art. 291 quarter of Presidential Decree 43/1973);

- other cases of smuggling (Article 292 of Presidential Decree 43/1973);

- penalty for smuggling in the event of failure or incomplete verification of the object of the crime (Article 294 of Presidential Decree 43/1973);

- failure to discharge the deposit bill. Differences in quantity (art. 305 of Presidential Decree 43/1973);

- differences in quality with respect to the deposit bill (art. 306 Presidential Decree 43/1973);

- differences in goods stored in private customs warehouses (Article 308 of Presidential Decree 43/1973);

- differences with respect to the declaration of goods intended for temporary import or export (310 Presidential Decree 43/1973);

- differences in quality in re-export to temporary import unloading (311 Presidential Decree 43/1973);

- differences in quality in the re-importation to temporary export discharge (312 Presidential Decree 43/1973);

- differences in quantity with respect to the declaration for re-export and re-importation (313 Presidential Decree 43/1973);

- failure to comply with the obligations imposed on captains (316 Presidential Decree 43/1973);

- non-compliance with customs requirements by aircraft captains (317 Presidential Decree 43/1973);

- penalties for violations of the regulations imposed on navigation in the surveillance areas (321 Presidential Decree 43/1973);

- All the cases introduced in the catalogue of predicate offences pursuant to Legislative Decree no. 141/2024 laying down supplementary national provisions to the Union Customs Code and revision of the system of penalties on excise duties and other indirect taxes on the production of consumption.

Offences committed with payment instruments other than cash and fraudulent transfer of values (Article 25-octies.1 of Legislative Decree 231/2001, as a result of Legislative Decree 184/2021 as a transposition of EU Directive 2019/713 as well as Legislative Decree 105/2023 converted into Law No. 137/2023 – provided for by Articles 493, 493-quarter, 640-ter and 512-bis of the Criminal Code):

- improper use, falsification or alteration, undue possession, transfer or acquisition of payment instruments other than cash to make a profit for oneself or for others (Article 493 of the Criminal Code);

- possession and dissemination of equipment, devices or computer programs aimed at committing crimes concerning payment instruments other than cash (Article 493-quarter of the Criminal Code);

- alteration of the functioning of a computer or telematic system or intervening without right in any way on data, information and programs contained in a computer or telematic system or pertaining to it, procuring for oneself or others an unfair profit with damage to others through a transfer of money of monetary value or virtual currency (aggravating circumstance 640-ter of the Criminal Code);

- any other crime against public faith or against property that has as its object payment instruments other than cash, unless it constitutes an administrative offence sanctioned more seriously.

Crimes against animals referred to in art. 25-undevicies of Legislative Decree no. 231/2001, such as:

- killing of animals (Article 544 bis of the Criminal Code);

- mistreatment of animals (Article 544 ter of the Criminal Code);

- prohibited shows or events (Article 544 quarter of the Criminal Code);

- prohibition of animal fights (Article 544 quinquies of the Criminal Code);

- killing or damaging other people's animals (Article 638 of the Criminal Code).

Of the introduction in the 231 catalogue of the offences referred to in Law no. 22 of 9 March 2022:

- 1. crimes against cultural heritage (art. 25-sepriesdecies of Legislative Decree 231/2001) which include:

- violation of the alienation of cultural property (Article 518-novies of the Criminal Code);

- embezzlement of cultural property (Article 518-ter of the Criminal Code);

- illegal importation of cultural property (Article 518-decies of the Criminal Code);

- illegal exit or export of cultural property (Article 518-undecies of the Criminal Code);

- destruction, dispersion, deterioration, disfigurement, soiling and illegal use of cultural and landscape heritage (Article 518-duodecies of the Criminal Code);

- counterfeiting of works of art (Article 518-quaterdecies of the Criminal Code);

- theft of cultural property (Article 518-bis of the Criminal Code);

- receiving stolen cultural property (Article 518-quarter of the Criminal Code);

- forgery in private deeds relating to cultural heritage (Article 518-octies of the Criminal Code).

- laundering of cultural property and devastation and looting of cultural and landscape heritage (art. 25-duodevicies of Legislative Decree 231/2001).

1.2. Penalties

The sanctions for the Company provided for by the Decree for administrative offences dependent on crime are:

- financial penalties;

- disqualification sanctions;

- confiscation;

- publication of the judgment.

In particular, the disqualification sanctions consist of:

- prohibition from exercising the activity;

- prohibition of contracting with the public administration;

- the suspension or revocation of authorizations, licenses or concessions functional to the commission of the offense;

- exclusion from facilitations, financing, contributions and subsidies, and/or the revocation of those already granted;

- prohibition of advertising goods or services.

1.3. Initiatives that exempt the Company

The Decree, in introducing the administrative liability of the Entity, however, provides for a form of exemption from such liability if the Entity demonstrates that it has adopted all the appropriate and necessary organizational measures to prevent the commission of crimes by subjects operating on its behalf.

In particular, the Company is exempt from liability if it proves that:

- the management body has adopted and effectively implemented, before the commission of the act, an organisational and management model suitable for preventing offences of the kind that occurred;

- the task of supervising the operation and compliance with the Model as well as proposing its updating has been entrusted to a Supervisory Body, endowed with autonomous powers of initiative and control;

- the persons committed the crime by fraudulently circumventing the Model;

- there has been no omission or insufficient supervision by the Supervisory Body.

In light of the above, it is essential for the Company to create and effectively adopt an Organization, Management and Control Model, i.e. a document with which the Company regulates its operation in order to prevent its employees and collaborators from committing the crimes provided for by Legislative Decree no. 231/2001.

02. GUIDELINES

The preparation of this Model is inspired by the Guidelines issued by Confindustria.

According to the aforementioned Guidelines, the process of adopting a 231 prevention system must take place following these fundamental steps:

- identification of "risk areas", aimed at verifying in which business areas/sectors it is possible to commit the crimes referred to in the Decree;

- preparation of a "control system" capable of preventing risks through the adoption of special protocols.

The founding elements of the preventive control system are:

- code of ethics;

- organizational systems;

- manual and computer procedures;

- authorization and signature powers;

- control and management systems;

- communications to staff and their training.

The control system must also be based on the following principles:

- verifiability, documentability, consistency and congruence of each operation;

- separation of duties;

- documentation of controls;

- introduction of an adequate sanctioning system for violations of the law and procedures provided for by the Model;

- identification of a Supervisory Body;

- information obligations on the part of the Supervisory Body and towards it.

03. THE ADOPTION OF THE MODEL BY SAVAR S.R.L.

3.1. The Company

Savar S.r.l. (hereinafter also "Savar" or the "Company") is active in the production of industrial technical ceramics and has specialized, in particular, in the production of pressed and drawn ceramic insulators for electrical resistance supports.

Since 1977, the year of its establishment, Savar has constantly invested in the development and research of new materials in order to create increasingly high-performance products. This with the aim of providing its customers with the best possible service. In this regard, Savar, in order to meet the specific needs of the customer, carries out ad hoc productions based on the design provided by the customer.

The Company is administered by a Board of Directors with all the powers of ordinary and extraordinary administration.

3.2. The Company's motivations for adopting the Model

Savar's Organization, Management and Control Model (the "Model"), aims not only to create a system of rules and procedures aimed at preventing, as far as reasonably possible, the commission of crimes but also to make all those who act in the name and on behalf of the Company (whether or not they belong to the company's staff) informed. the consequences that may derive from conduct that does not comply with those rules and the possibility of committing crimes, which results in the application of sanctions, for the offender and the Company, pursuant to the Decree.

The Model therefore intends to raise awareness among the Company's personnel, external collaborators and partners, reminding them to behave correctly and transparently, to comply with the precepts defined by the Company and contained in the Model, and to comply with all rules and procedures.

From this point of view, the Model forms, together with the Code of Ethics, an organic corpus of internal rules and principles, aimed at spreading a culture of ethics, fairness and legality.

In drafting the Model, the Company aligned itself with the guidelines of Confindustria, in the updated version of June 2021. The Model was adopted by the Company by resolution of the Board of Directors and is updated and amended on the occasions and in accordance with the procedures set out in paragraph 3.10.

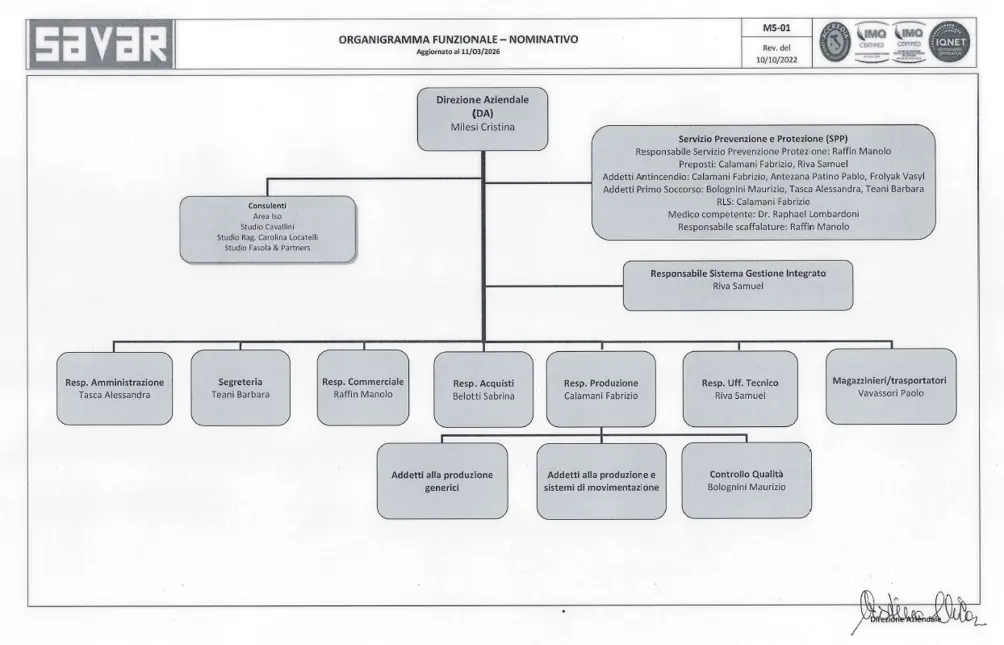

The Company's organisational chart in place at the date of preparation of this document is shown below.

3.3. The Quality, Health and Safety Policy

For risk prevention purposes, the Company has also adopted an internal management system compliant with ISO standards, obtaining the relevant certifications relating to the ISO 45001:2018 Occupational Health and Safety Management System and the ISO 9001:2015 Quality Management System.

This Model, therefore, complies with the provisions of art. 30 of Legislative Decree no. 81/2008.

In drafting the Model, Savar integrated these management systems with the provisions of the Decree, the aforementioned Guidelines and the best practices and policies adopted by the Company.

In this regard, the principle referred to in art. 30 paragraph 5 of Legislative Decree no. 81/2008 in the field of health and safety prevention. This Model therefore complies with the requirements of the aforementioned standard.

The Company therefore pursues a quality, health and safety management policy with the primary objective, supported by all its collaborators, to increase the market position of its organization, to obtain continuous improvement and continuous satisfaction of its customers, operating in a quality and occupational health and safety regime, in accordance with the aforementioned certifications.

The Company has therefore entrusted the role of Head of the Management System to a person competent in the sector and in the regulations, with the task of disseminating, supporting and maintaining the Management System itself.

The Head of the Management System, supported as necessary by the competent functions, has as his primary objective to monitor and suggest interventions aimed at improving the performance of the organization and understanding, disseminating and respecting principles such as:

- Customer focus

- Leadership

- the active participation of all collaborators (each according to their competence)

- relationship management

- The process approach

- evidence-based decision-making

- respect for the environment

Savar therefore assumes, among others, the following priority commitments that the entire organization makes its own:

- Observe and enforce all applicable laws and regulations specific to the business

- systematically detect the impacts of activities on environmental and health and safety issues, understand their effects and prevent and identify their causes

- identify and manage accidents and near misses, drawing from the latter ideas for improvement

- plan objectives and related goals

- implement the defined programs, continuously monitor the progress of these goals, implement programs aimed at reducing, where possible, energy and raw material consumption, containing pollution and minimizing the environmental impacts deriving from its activities, using materials with the longest possible life cycle

- to have waste managed in a way that favors activities such as recovery and recycling instead of disposal

- achieve the satisfaction of the organization's employees, through

a. adequate and constant training that covers business issues, activities, health and safety, quality and the environment

b. an increase in professional competence and awareness of the importance of the role played within the company system

c. company structures suitable for the activities

- establish a climate that contributes to maintaining a negligible level of absenteeism

- involve suppliers who are required to collaborate in compliance with the principles of the policy

- promote and seek to achieve an open dialogue with local communities and environmental authorities

- introduce control and audit methodologies of its management system

- implement, update, one's own management system support processes with the right availability of resources

- seek the continuous satisfaction of customers, through an analysis of their needs, the achievement of the level "0" objective of the index of complaints, a careful selection of its suppliers, supply of products at an increasingly high quality level, in compliance with the commitment to work for continuous improvement

- the maintenance of certification for the UNI EN ISO 9001 and UNI ISO 45001 standards, with timely reviews of the system that must include checks on the improvement of individual processes, the adequacy of the policy and the objectives for quality and the environment.

These commitments are implemented through company objectives, targets and programmes that are periodically established and reviewed.

This Policy is communicated to all personnel working under the control of the organization in order to make them aware of the contents of the same and verify the level of understanding.

The Company, through the Quality Safety Manager, is required to provide the Supervisory Body with an annual report in January of each year relating to any additions or changes to internal procedures, improvements and maintenance activities of machinery and structures or problems that have occurred.

3.4. The basic principles of the Model

The purpose of the Model is represented by the construction of a control system aimed at preventing certain crimes such that it cannot be violated except by fraudulently circumventing the procedures contained therein.

To this end, the Model refers to all the company rules/procedures existing on the date of its entry into force and will be integrated with those that will be introduced later.

The Model, therefore, performs the following functions:

- make all those who work in the name and on behalf of the Company aware of the need to comply with the provisions of the Model, the violation of which results in severe disciplinary sanctions;

- inform the Company of the consequences that may arise from the application of the financial and disqualification sanctions referred to in the Decree, sanctions that may also be ordered as a precautionary measure;

- allow the Company, on a preventive basis, constant control and careful supervision of its activities.

In the creation of the Model, the Company's business context was first analysed in order to identify in which area/sector of activity and in what ways there is a risk of committing crimes.

To this end, a prior examination of the company documentation was conducted (organization charts, powers of attorney, activities carried out, organizational provisions, etc.) and a series of interviews with the subjects in charge of the various sectors of the company, in order to verify the existing risks as well as the forms of control already prepared (existing procedures, separation of functions, traceability of controls, etc.). In this phase, particular attention was paid to (i) the identification of the processes for the management and control of financial resources; (ii) the processes relating to the preparation of accounting records and their storage; (iii) the process of quantifying the tax obligation; (iv) the process of appointing consultants; (v) environmental issues; (vi) health and safety issues; (vii) the provision of sponsorship, donations, gifts and gifts; (viii) the management of relations with suppliers, (ix) the management of the active and passive cycle; (x) the management of authorizations and (xi) the management of foreign counterparties.

The Model prepared by the Company is based on an internal regulatory system aimed at planning the formation and implementation of the Company's decisions on the risks/crimes to be prevented through:

- the principles of conduct contained in the procedures and in the Code of Ethics;

- a risk assessment process aimed at identifying the areas and procedures at risk in relation to the company structure;

- a system of delegation of functions and powers of attorney for the signing of company deeds that ensures a clear and transparent representation of the process of formation and implementation of decisions (as already provided for by the governance system adopted by the Company);

- the appointment of the Supervisory Body responsible for supervising the operation and compliance with the Model and proposing its updating;

- the provision of a disciplinary system suitable for sanctioning non-compliance with the measures indicated in the Model and in the Code of Ethics.

3.5. The structure of the model

This Model consists of:

- a general part (which sets out the general principles of the control system and its essential components);

- a special part containing the control protocols, i.e. for each sensitive activity:

a. the recipients;

b. the roles and responsibilities of the subjects/functions involved;

c.la description of the process;

d. the principles of conduct;

e. information flows.

3.6. Risk analysis

The risk analysis has the function of identifying which are the business areas/processes in which it is possible, in practice, to commit the crimes provided for in the Decree, as well as allowing preparatory activities to be carried out for the identification of the relevant rules of conduct and control.

This analysis is carried out through:

- examination of company organizational charts and relevant documentation (e.g.: system of proxies and powers of attorney, operating procedures and instructions, etc.);

- cycle of interviews with subjects operating in the company structure in order to identify areas potentially at risk.

The risk of committing 231 offences relating to the business areas considered is analysed in detail in the risk assessment documents referred to above.

The results were submitted for approval to the parties involved, who participated in the meetings, according to their competence, in order to become aware of the risks inherent in the activities they are responsible for and, consequently, to make them responsible.

Finally, it should be noted that the risk assessment activity considered the types of offences compatible with the Company's activities and concretely envisaged.

From the risk assessment activity, it emerged that within Savar, the activities potentially at risk of committing predicate crimes are the following:

- management of purchases and the passive cycle;

- management of the active cycle;

- management of financial flows;

- extraordinary transactions;

- preparation of accounting records and financial statements;

- storage of accounting documentation;

- management of tax returns and quantification of tax obligations;

- selection of suppliers and freight forwarders;

- management of commercial negotiations for the conclusion of purchase orders by customers;

- giving of gifts and gifts;

- relations with foreign counterparts;

- management of commercial relations with the Public Administration;

- management of disputes;

- management of the company's IT system;

- assignment of consultancy;

- personnel selection and management;

- management of inspection visits and authorizations;

- management of health and safety obligations;

- management of environmental obligations.

3.7. Control Protocols

After identifying the areas and processes at risk, a protocol was defined for each sensitive activity.

The protocols contain the most suitable discipline to govern the identified risk profile, i.e. a set of rules originating from a detailed analysis of each individual activity and the related risk prevention system.

In particular, for each sensitive activity, the following have been described:

- the scope of the protocol;

- the roles and responsibilities of the subjects/functions involved in the performance of the processes;

- the characteristic phases of carrying out the activities;

- the principles of conduct to which the recipients of the protocol must comply in carrying out the activity itself;

- information flows.

The protocols were submitted to the examination of the parties responsible and, in particular, to the Board of Directors, for their evaluation and approval.

The protocols are communicated to the recipients of the Model through a service communication, thus making the rules of conduct contained therein binding and mandatory for all those who find themselves carrying out the activity in which a risk profile has been identified.

The definition of the protocols is completed and integrated with the Code of Ethics and the procedures that the Company has adopted, as described in the following paragraph.

3.8. The Code of Ethics and internal procedures

The ethical and behavioural principles to which the Company adheres are defined in the Code of Ethics adopted by resolution of the Board of Directors on 4.02.2019.

The Code of Ethics is an instrument adopted independently and susceptible to general application by Savar in order to express the principles of "corporate ethics" that the Company recognizes as its own and on which it calls for compliance by all people, without exception, linked to it by employment and/or collaboration relationships.

The Company is also equipped with:

- internal procedures;

- procedures adopted as part of the ISO 45001:2018 certified occupational health and safety Management System and within the ISO 9001:2015 certified Quality Management System;

- procedures adopted as a result of the risk assessment activity aimed at overseeing the sensitive activities most exposed to the risk of committing crimes.

3.9. The recipients of the Model

This Model is intended for all personnel of Savar S.r.l.: the provisions contained therein must, therefore, be complied with both by the managerial staff who work in the name and on behalf of the Company and by all employees of Savar and this according to the degree of responsibility assigned to them.

In any case, it is understood that the Company's employees will be appropriately trained and informed of the contents of the Model, in accordance with the procedures indicated in the same.

As far as the Company's internal collaborators are concerned, however, they will be appropriately trained, and informed of the contents of the Model, according to the methods indicated in the same.

On the other hand, with regard to the Company's external collaborators, understood both as natural persons (consultants, professionals, etc.) and as legal persons who collaborate with Savar, compliance with the principles of the Model that govern the Company's action is guaranteed through the definition of contractual clauses that require compliance with the Code of Ethics and the Savar Model or, conversely, that the policyholder declares that it has adopted its own Model and its own code of ethics whose principles it declares to be consistent with those of similar documents of the Company.

3.10. Amendments and additions to the Model

The Decree expressly provides for the need to update the Model in order to keep it constantly in line with the specific needs of the Entity and its concrete operations.

The adaptation and/or updating of the Model will be carried out at least on the occasion of:

- regulatory innovations;

- violation of the Model and/or negative results of checks on its effectiveness;

- changes in the Company's organisational structure.

The Board of Directors is responsible for updating the Model, and therefore for its integration and/or amendment, which may consult with the other competent structures/functions.

Any substantial change, relating, for example, to the introduction of new special parts or new protocols in company areas at risk, requires prior consultation with the Supervisory Body.

Minor changes, i.e. formal changes, such as, for example, the alignment of protocols with new organisational provisions, can be made directly by management, subject to agreement with the Supervisory Body, followed by ratification by the Board of Directors.

The simple "care" of updating the Model, i.e. the mere solicitation in this sense and not its direct implementation, is instead the responsibility of the Supervisory Body.

With reference to the company rules/operating instructions/procedures/protocols referred to in the Model or to those which, although referred to, regulate the processes referred to in the areas at risk, any modification, integration, elimination, etc., must be communicated by the competent function to the Supervisory Body, in order to analyse any impacts on the internal control system, relevant for the purposes of 231.

4. SUPERVISORY BODY

4.1. Identification of the Supervisory Body

According to the provisions of the Decree, the characteristics of the Supervisory Body must be those of:

- autonomy and independence, fundamental requirements so that the Body is not directly involved in the management activities that represent the object of its supervisory activity.

To this end, the Body must be appointed by the Board of Directors and the members of the Board of Directors must not have operational tasks within the company.

The Body must be endowed with decision-making autonomy and autonomous spending power.

The Board of Directors, on the proposal of the Supervisory Body, will allocate to the Board an endowment fund, which the Supervisory Body may request to be supplemented in the event of justified needs. The position of the SB within the Company must guarantee the autonomy of the control initiative from any form of interference and/or conditioning by any body (and in particular the management body);

- professionalism, understood as the possession of technical and professional skills appropriate to the control functions that the body is required to perform;

- continuity of action, to this end the body must:

a. ensure the updating of the Model;

b. constantly supervise the application of the Model, exercising the necessary investigative powers for this purpose;

c. represent a constant reference for all the Company's personnel and, in general, for all recipients of the Model.

Therefore, in order to ensure the continuity of supervisory activities, the body must be a body of the Company which must not compete with operational or managerial tasks capable of influencing the overall vision of the company's activities.

In carrying out its duties, the Supervisory Body will make use of the support of other Savar corporate functions and/or external consultants, according to the skills that will be necessary on a case-by-case basis.

4.2. Composition and appointment of the Supervisory Body

The Supervisory Body can have a monocratic or collegial composition; The choice of the composition is left to the administrative body.

The members of the body remain in office for the duration defined by the Board of Directors at the time of appointment and may always be re-elected.

Their replacement before the expiry of the mandate can only take place for just cause or justified reason, meaning as such, by way of example:

- voluntary renunciation by the member of the body;

- supervening incapacity due to natural causes;

- the failure to meet the requirements of good repute;

- the loss of the requirement of independence;

- failure to attend two or more meetings, even non-consecutive, without justified reason within twelve months;

- failure by a member of the body to notify the Board of Directors of the occurrence of a cause for forfeiture referred to in the following paragraph;

- the occurrence of one of the causes of suspension or revocation referred to in the following paragraph.

The Board of Directors of Savar S.r.l. establishes, for the entire duration of the office, the annual remuneration due to the members of the Supervisory Body.

Internal members, if appointed, do not receive any additional compensation.

4.3. Grounds for ineligibility, forfeiture, suspension, dismissal of members of the supervisory body

Those who meet the conditions provided for by Article 2382 of the Italian Civil Code cannot be appointed as members of the Supervisory Body.

In addition, in order to hold the position of member of the supervisory body, the subjects must declare:

- not to have kinship, marriage or affinity relationships within the fourth degree with members of the Board of Directors, nor with top management in general;

- that there are no conflicts of interest, even potential, with the Company such as to jeopardise the independence required by the role and duties of the Supervisory Body;

- that he/she does not hold, directly or indirectly, shareholdings of such an entity as to allow him to exercise significant influence over the Company;

- not to hold and not to have held administrative functions – in the three financial years prior to his appointment as a member of the Supervisory Body – of companies subject to bankruptcy, compulsory administrative liquidation or other insolvency proceedings;

- not to have been part of public employment relationships with central or local administrations in the three years prior to their appointment as a member of the Supervisory Body;

- that he/she has not held the position of member of the Supervisory Body within companies against which sanctions have been applied pursuant to Article 9 of Legislative Decree 231/2001 and subsequent amendments and additions;

- that he/she has not been convicted - even if it has not become final or issued pursuant to Article 444 et seq. of the Code of Criminal Procedure and even if with a conditionally suspended sentence, without prejudice to the effects of rehabilitation - or, a measure that in any case ascertains one's liability, in Italy or abroad, for the crimes referred to in Legislative Decree no. 231/2001 or similar crimes;

- that he/she has not been convicted, even with a sentence that has not become final or issued pursuant to Article 444 et seq. of the Code of Criminal Procedure and even if with a conditionally suspended sentence, without prejudice to the effects of rehabilitation - or with a measure that in any case ascertains his/her liability, to a penalty that imposes the interdiction, even temporary, from public offices, or temporary disqualification from the management offices of legal persons and companies;

- that he/she has not been definitively the recipient of one of the prevention measures provided for by Legislative Decree no. 159/2011 containing "Code of anti-mafia laws and prevention measures, as well as new provisions on anti-mafia documentation, pursuant to articles 1 and 2 of law no. 136 of 13 August 2010".

Candidates for the office of members of the Supervisory Body must self-certify, with a declaration in lieu of notoriety, that they do not meet any of the conditions indicated from numbers 1 to 9, expressly undertaking to communicate any changes with respect to the content of these declarations.

The members of the Supervisory Body lose their office and may consequently be removed from office when they find themselves after their appointment:

- in one of the situations contemplated in art. 2399 of the Italian Civil Code;

- in one of the conditions indicated in numbers 1-9 of the conditions of ineligibility indicated above;

- in the situation in which, after the appointment, it is ascertained that he or she has held the position of member of the Supervisory Body within a Company against which the sanctions provided for by art. 9 of the Decree in relation to administrative offences committed during their office;

- in the event of the application of a personal precautionary measure;

- in the event of provisional application of one of the preventive measures provided for by art. 10, paragraph 3, of Law No. 575 of 31 May 1965, as replaced by Article 3 of Law No. 55 of 19 March 1990, as amended;

- in the event of ascertainment, by the Board of Directors, of negligence, incompetence or gross negligence in the performance of the tasks assigned pursuant to the following paragraph and, in particular, in the identification and consequent elimination of violations of the Model, as well as, in the most serious cases, the perpetration of crimes.

4.4. Functions and powers of the Supervisory Body

In order to supervise the application of the Model and to verify its effectiveness, the SB is entrusted with the following tasks:

- coordinate with the various heads of the corporate functions with regard to the implementation of the Model. To this end, the Body, in cooperation with the company departments concerned, must promote suitable initiatives for the dissemination and understanding of the Model, for staff training, for the definition of standard contractual clauses, etc.;

- coordinate with the various managers of the other corporate functions in order to prepare the internal organisational documentation, containing instructions, clarifications or updates, necessary to ensure the functioning of the Model;

- collect and store relevant information regarding compliance with the Model. To this end, the Body has free access to all company documentation and all communications of an organisational and/or managerial nature must be forwarded to it;

- periodically check the map of areas at risk of crime;

- verify the effective application of the company procedures and protocols adopted by the Company in the areas at risk and this in order to prevent the commission of crimes;

- verify certain specific transactions or acts particularly exposed to the risk of crime. The checks can be carried out either as part of a pre-established verification plan or through "surprise checks";

- prepare tools intended to receive from the recipients of the Model any requests for clarification regarding problematic hypotheses as well as requests for interventions aimed at ensuring the correct monitoring of the Model;

- verifying the coordination of the Model with the ISO Management Systems adopted by the Company;

- take care of the updating and integration of the Model whenever regulatory, implementation or organizational needs require it.

In order to carry out the aforementioned tasks, the Body:

- it may define its own operating regulations, communicating them, in the event of adoption, to the Board of Directors;

- must have free access to all company documentation;

- may obtain statements from persons who can provide information relevant to the operation of the Model;

- it can give impetus to disciplinary proceedings;

- has adequate financial resources in order to be able to properly carry out its tasks.

4.5. Reporting by the Supervisory Body

Savar's Supervisory Body is assigned three reporting lines:

- the first on an ongoing basis, directly to the Chief Executive Officer and the Legal Representative;

- the second, on an annual basis, towards the entire Board of Directors.

The Body may be convened at any time by the aforementioned bodies and functions and may, in turn, request their convocation when it deems it necessary to report on compliance with the Model.

4.6. Information flows to the Supervisory Body

In order to facilitate the supervision of the effectiveness of the Model, all organisational and/or managerial information deemed useful for this purpose must be transmitted to the Body, including observations on the adequacy of the control system adopted.

Each responsible party is required to transmit to the Supervisory Body all the information identified and defined in the protocols referred to in the Special Part of this Model.

The Supervisory Body may, in any case, ask the recipients of the Model for information, additions and/or documents for the complete and correct performance of its activities.

The communications referred to in this paragraph must be promptly sent to the following e-mail address: segnalazioni@fasolaw.it. It should be noted that only the members of the SB have access to this e-mail address, who will follow up on the communications received, guaranteeing the confidentiality of the data of the authors of the communications, without prejudice to legal obligations.

The Company shares with the Supervisory Body the minutes of the Management Review held in relation to the quality system adopted, in order to coordinate the risk control requirements pursuant to this MOGC with those provided for by the Management Systems.

The Head of the Integrated Management System must inform the SB regarding:

- the evaluations conducted as part of the Integrated System Analysis;

- changes and updates to the Safety and Quality Policy and the related program;

- the results of audit activities and periodic verification of legislative compliance;

- the results of the verification activities by the certifiers;

- the implementation of the actions identified in the safety and quality programme.

05. WHISTLEBLOWING REPORTS

In implementation of the provisions of art. 6 paragraph 2-bis of Legislative Decree no. 231/2001, the following channels are established through which the persons indicated in Article 5, paragraph 1, letters a) and b) of the Decree may submit, in order to protect the integrity of the Company, detailed reports of unlawful conduct relevant to the Decree and based on precise and consistent factual elements or violations of the Model of which they have become aware due to the functions performed:

- by closed mail addressed to the SB c/o the Company's registered office;

- by e-mail addressed to the reserved mailbox segnalazioni@fasolaw.it.

Additional and different channels may be set up by the Company, which in this case will provide adequate information to the interested parties.

All reports received through the aforementioned channels are transmitted to the SB and managed in a manner that guarantees the confidentiality of the identity of the whistleblower in the management of the report and in compliance with the legislation on Privacy.

All reports received are evaluated by the SB; Vague, unsubstantiated reports that do not refer to precise and concordant factual elements, or that are clearly made in bad faith or have slanderous or defamatory content, will not be taken into consideration.

Anonymous reports, i.e. without elements that allow their author to be identified, provided that they are delivered in the manner provided for in this document, will be taken into consideration by the SB, if they are adequately detailed and rendered in great detail, i.e. they are such as to bring out facts and situations in relation to specific contexts (e.g. indications of names or particular qualifications, mention of specific offices, particular procedures or events, etc.).

5.1 Protection of the whistleblower and the parties involved

Maximum protection of the confidentiality of the identity of the authors of the reports conveyed through the whistleblowing channel is guaranteed, ensuring the same protection to all persons mentioned and/or in any case involved in the report, without prejudice to legal obligations and the protection of the rights of the Company and/or of the persons wrongly accused and/or in bad faith.

The maximum confidentiality of the content of the report is also ensured.

To guarantee compliance with the obligation of confidentiality, Savar has provided for the application of disciplinary sanctions against those who are found to be responsible for the violation of this obligation, as better explained in paragraph 8 below.

It should be noted that the application of retaliatory measures against subjects protected by the legislation (such as reporting subjects) must be the subject of a report conveyed through the external reporting channel set up at the institutional website of ANAC: it will then be the latter that will report it to the national labour inspectorate.

It should be noted, however, that reports must be made in good faith, must be substantiated with precise information and be corroborated by elements that are not manifestly unfounded. In fact, the mechanisms for the protection of the whistleblower do not apply in the case of ascertainment by sentence of criminal liability for the crimes of slander or defamation or in any case for the same crimes committed with the complaint, or of civil liability, for having reported false information made with intent or gross negligence.

In cases where such responsibilities are ascertained, a disciplinary sanction shall be applied to the whistleblower as specified in paragraph 8 below.

06. STAFF TRAINING

6.1 Staff training and information

Savar promotes knowledge of the Model and its protocols among all employees, who are required to know its content and contribute to its implementation.

To this end, the Company defines, at a frequency to be determined by the Board of Directors after consultation with the Supervisory Body, a specific communication and training plan aimed at illustrating the Model and the special parts to all personnel, within which the activities to be carried out are indicated and the possibility of making changes and additions during the year is envisaged.

6.2. Communications to staff

There are several moments in the life of the Company in which communications regarding the Model are made.

In particular, an initial dissemination activity is carried out, during which all employees are informed of the adoption of the Model by the Company and, subsequently, further communications are made both to periodically raise awareness among employees and to communicate updates to the Model, procedures, codes, etc.

As far as communication is concerned, the following alternative methods are envisaged:

- the dissemination of the Model through the company information systems and its sending by e-mail to all employees with PCs;

- the dissemination of the Model through the use of the company bulletin board, for all employees who do not have a PC;

- Update emails.

In addition, new hires will be informed at the time of hiring, of the existence of the Model and its main contents and will sign a form for acknowledgment and acceptance of the Model itself, with which they must undertake, in the performance of their duties, to comply with the principles, rules and procedures contained therein.

6.3 Training activities

The training activity aimed at disseminating knowledge of the regulations referred to in the Decree is differentiated, in terms of content and delivery methods, according to the qualification of the recipients, the level of risk of the area in which they operate and whether or not they have representative functions of the Company. Training sessions can be carried out either in e-learning mode or through classroom sessions. In both cases, attendance at the lessons must be kept in track.

6.4 Information to external collaborators and partners

In order to promote knowledge and compliance with the Model also among its consultants, collaborators, customers and suppliers, the Company will provide specific information on the principles and procedures that Savar has adopted on the basis of the Model as well as the contractual clauses that will be adopted by the Company as a result.

07. THE SYSTEM OF POWERS OF ATTORNEY AND DELEGATIONS

For the granting, management and revocation of powers of attorney attributing powers of representation, the Company requires that:

- the limitations of power provided for the Chief Executive Officer in the delegation conferred on him by the Board of Directors are complied with;

- the limitations of power provided for the Chief Executive Officer and the Legal Representative with regard to acts of extraordinary administration are complied with;

- the limitations provided for the exercise of the so-called Banking Powers (powers to maintain contractual relations with credit institutions) are complied with.

08. DISCIPLINARY SYSTEM

The preparation of an adequate sanctioning system for the violation of the provisions contained in the Model and the Code of Ethics, as well as the provisions of the Management Systems adopted by the Company, is an essential condition to ensure their effective implementation. Savar's disciplinary system is adopted pursuant to art.6, second paragraph, letter E) and art. 7, fourth paragraph, letter b) of the Decree.

The rules contained in the Model will be an integral part of the company regulations and consequently their violation will constitute a serious disciplinary offence, supplementing the provisions of art. 2106 of the Italian Civil Code, by the procedures and rules provided for by the collective agreements in force.

The rules of conduct imposed by the Model are assumed by Savar to be fully autonomous, the application of disciplinary sanctions is therefore independent of the outcome of any criminal proceedings. Conduct by workers in violation of the rules contained in this Model is therefore considered disciplinary offences. The entry into force and dissemination of this Model will constitute publication of the rules contained therein with the consequence that from that moment on, discrepancies can be detected and penalties imposed.

8.1. Imposition of penalties

The procedure for imposing sanctions takes place in accordance with the contractual provisions and regulations provided for in the field of labour.

In particular, it is the duty of the Supervisory Body to report violations of the relevant body of legislation for the purposes of 231 of which it becomes aware to the Chief Executive Officer, to initiate the sanctioning procedure in compliance with the law and the sector's national collective bargaining agreement, subject to:

- timely and detailed complaint of the violation to the worker;

- analysis of the justifications given by the worker;

- investigation and investigation into the incident.

The Chief Executive Officer defines, on a case-by-case basis, the type and extent of the sanctions to be imposed, in proportion to the seriousness of the shortcomings and, in any case, in consideration of the elements listed below:

- subjective element of the conduct, depending on the intent or negligence;

- relevance of the obligations violated;

- level of hierarchical and/or technical responsibility;

- presence of aggravating or mitigating circumstances with particular regard to professionalism, previous work experience, circumstances in which the act was committed;

- possible sharing of responsibility with other parties who have contributed to determining the violation;

- conduct that may compromise, albeit potentially, the effectiveness of the Model.

Disciplinary sanctions are also imposed, in the same manner, on those who are found to be responsible:

- the violation of the obligation of confidentiality in the management of whistleblowing reports;

- the violation of the prohibition of retaliation against the whistleblower or other protected subjects pursuant to Legislative Decree no. 24/2023;

- to have obstructed or attempted to obstruct the submission of the report;

- the failure to establish channels and procedures for the submission and management of reports in accordance with applicable legislation;

- that it has not carried out the verification and analysis of the reports received;

- for the crimes of slander or defamation or in any case for the same crimes committed with the complaint, or civil liability, for having reported false information intentionally reported with intent or gross negligence, responsibility ascertained by judgment.

8.2. Sanctioning system for employees

Conduct by employees in violation of the principles of conduct and protocols indicated in the Model constitutes disciplinary offences.

Only the sanctions provided for by the applicable CCNL may be imposed on employees, in compliance with the procedures indicated in Article 7 of the Workers' Statute and any special regulations applicable on the subject.

In relation to the above, the Model expressly refers to the sanctioning system provided for in the sector's national collective bargaining agreement for disciplinary violations.

In particular, given the principle of typicality of disciplinary violations and sanctions, disciplinary measures are identified for workers linked to the Company by a relationship of subordination, the disciplinary measures are indicated in art. 238 of the National Collective Labour Agreement for the trade sector.

In detail, it is expected that:

- a worker who violates the principles of conduct and protocols indicated in the Model (e.g. who does not comply with the prescribed procedures, fails to communicate the prescribed information to the SB, fails to carry out checks, fails to report any risk situations relating to health and safety in the workplace to the Prevention and Protection Service) incurs written reprimand, fine or suspension , does not use or makes inadequate use of Personal Protective Equipment, fails to report risky situations relating to the protection of the environment, etc.) o adopts, in carrying out activities in risky processes, conduct that does not comply with the requirements of the Model itself;

- In addition, the dismissal with notice is also incurred by the worker who:

a. adopts in carrying out activities in risky processes a behaviour that does not comply with the provisions of this Model and is unequivocally aimed at committing an offence sanctioned by the Decree or, with specific reference to health and safety issues,

b. does not continuously carry out the supervisory activity prescribed pursuant to the Consolidated Law 81/2008 on health and safety at work

c. implements obstructive behaviour towards the SB or the subjects (i.e.: Employer, Head of the Prevention and Protection Service, RLS or other subjects of the organisation chart referred to in the Risk Assessment Document pursuant to Consolidated Law 81/2008) responsible for the Occupational Health and Safety management system;

- finally, the measure of dismissal without notice is also incurred by the worker who, in the performance of the activities in the processes at risk, behaves in a way that is clearly in violation of the provisions of this Model, such as to determine the concrete application to the Company of the measures provided for by the Decree or, with specific reference to health and safety issues, repeatedly tampers with the machinery and/or equipment and/or the Personal Protection thus causing danger to oneself or others.

The ascertainment of the aforementioned infringements, possibly upon notification by the Supervisory Body and/or the employer in the event of infringements of the occupational health and safety system, the management of disciplinary proceedings and the imposition of the sanctions themselves remain the responsibility of the Chief Executive Officer.

8.3. Sanctioning system for managers

In the event of violations by managers of the internal procedures provided for in this Model, the relationship of trust between the Company and the manager must be considered violated.

Consequently, the most appropriate measures will be applied to those responsible in accordance with the provisions of the national collective agreement applicable to them.

8.4. Sanctioning system for administrators

In the event of violation of the Model by the Company's directors, the competent person shall inform the Board of Directors and the supervisory body.

The same information will be provided to the Board of Directors and the control body if even one director has been responsible.

The Board of Directors will apply the sanction deemed most appropriate to the directors, according to the criteria illustrated in paragraph 8.1. that precedes. The Board of Directors has the right to impose fines, to revoke the powers conferred, as well as to convene the shareholders' meeting to resolve on the removal of the director.

In any case, in the event that the indictment of directors for offences deriving the administrative liability of the Company has been ordered, a shareholders' meeting will be convened to resolve on the most appropriate actions to be taken.

8.5. Sanctioning system for the members of the supervisory body

The same sanctions shall apply as provided for in the event of violation of the Model by the directors, as described in the previous paragraph, in the event of violation of the Model by the members of the supervisory body.

8.6. Sanctioning system for external collaborators

The company rules and those provided for by this Model will be communicated to external collaborators and partners of the Company, including commercial agents.

Any conduct carried out by external collaborators, partners and commercial agents in contrast with the guidelines indicated in this Model and such as to entail the risk of committing a crime provided for by the Decree may result in the application of the express termination clause that will be stipulated in each contract (except in any case for compensation for damages).

The Supervisory Body is responsible for the preparation, updating and inclusion in the letters of appointment or partnership agreements of these specific contractual clauses which will also provide for any compensation for damages suffered by the Company as a result of the application by the judge of the measures provided for by the Decree.

9. PROTOCOLS AND GENERAL PRINCIPLES

Corporate action must comply with certain general principles, regardless of the presence of a specific procedure. These principles, which are binding on all recipients, are:

- clear definition of powers and limits for persons operating in the name and on behalf of the Company;

- consistency between signing and organisational powers and related responsibilities, with particular regard to the system of powers of attorney and delegations;

- segregation of functions within each business process: there must be no subjective identity between those who decide, those who implement and those who control. In particular, a person responsible for each business process must always be identified;

- traceability of corporate activities: it must always be possible to reconstruct the phases of formation of the deeds and periodic reports must be provided by the managers of business processes on the most significant aspects of the activity carried out;

- traceability of financial flows: any transfer of financial resources, whether incoming or outgoing, must be precisely justified;

- monitoring: timely and periodic updating of powers of attorney, delegations as well as the control system;

- archiving: every company document relating to the formation and implementation of business decisions and every report must be archived by the Process Manager;

- there must always be compliance with the reference regulations together, where required, with the contents of the protocols relating to individual sensitive activities;

in relations with the P.A., the offer, giving or authorization, direct or indirect, of payments of sums of money or other value, in order to influence any action or decision by the operator belonging to the P.A., is prohibited;

10. PRELIMINARY CHECKS